Goes back to the Bernanke quotes from the Brookings link I posted last year: "inflation expectations… are an important determinant of realized inflation…."

Either you believe it or you don't. I believe it, apparently you don't. Life goes on.

Not sure how you can believe in something when you clearly don't understand how it works. (not saying I do)

it's sorta like religion

From the first paragraph in the first link I posted in this debate:

"Inflation expectations are simply the rate at which people—consumers, businesses, investors—expect prices to rise in the future. They matter because actual inflation depends, in part, on what we expect it to be. If everyone expects prices to rise, say, 3 percent over the next year, businesses will want to raise prices by (at least) 3 percent, and workers and their unions will want similar-sized raises."

I understand those three sentences. I'm not sure what's preventing you from understanding - I guess you need to do more reading.

Goes back to the Bernanke quotes from the Brookings link I posted last year: "inflation expectations… are an important determinant of realized inflation…."

Either you believe it or you don't. I believe it, apparently you don't. Life goes on.

Not sure how you can believe in something when you clearly don't understand how it works. (not saying I do)

it's sorta like religion

From the first paragraph in the first link I posted in this debate:

"Inflation expectations are simply the rate at which people—consumers, businesses, investors—expect prices to rise in the future. They matter because actual inflation depends, in part, on what we expect it to be. If everyone expects prices to rise, say, 3 percent over the next year, businesses will want to raise prices by (at least) 3 percent, and workers and their unions will want similar-sized raises."

I understand those three sentences. I'm not sure what's preventing you from understanding - I guess you need to do more reading.

"in part"

and what part is that? where are the supply chain issues? where are the rising costs based on rising fuel costs, which are impervious to expectations?

do people's expectations rise out of thin air or do they rise because inflation is going up?

my problem with expectations is that while their effect is probably a part of the inflation story, they are, as I've said before, immeasurable.

That last sentence in the quoted paragraph really doesn't make any sense. It conflates causes and effects. It implies that prices will rise to compensate for increasing labor costs. What happens if the rising labor costs don't happen - as has been the case for decades. Should inflation then get rolled back?

And do you really think you can adequately describe the economics of labor in the US by saying "If everyone expects prices to rise, say, 3 percent over the next year, businesses will want to raise prices by (at least) 3 percent, and workers and their unions will want similar-sized raises." Are those 3 percent raises inevitable for everyone, or even a majority? Of course they're not. What industries are more likely to get them over others? How do those industries tie in to our consumer costs?

My problem with your push for expectations is that your view is crazy simple - exemplified by what you quoted. If you think that quote actually describes the mechanisms by which expectations have affected recent inflation, well then, we're done.

good piece by Claudia Sahm, former economist for the Fed

I liked this paragraph, including the linked article by Skanda Amarnath. Leave her in, Coach!

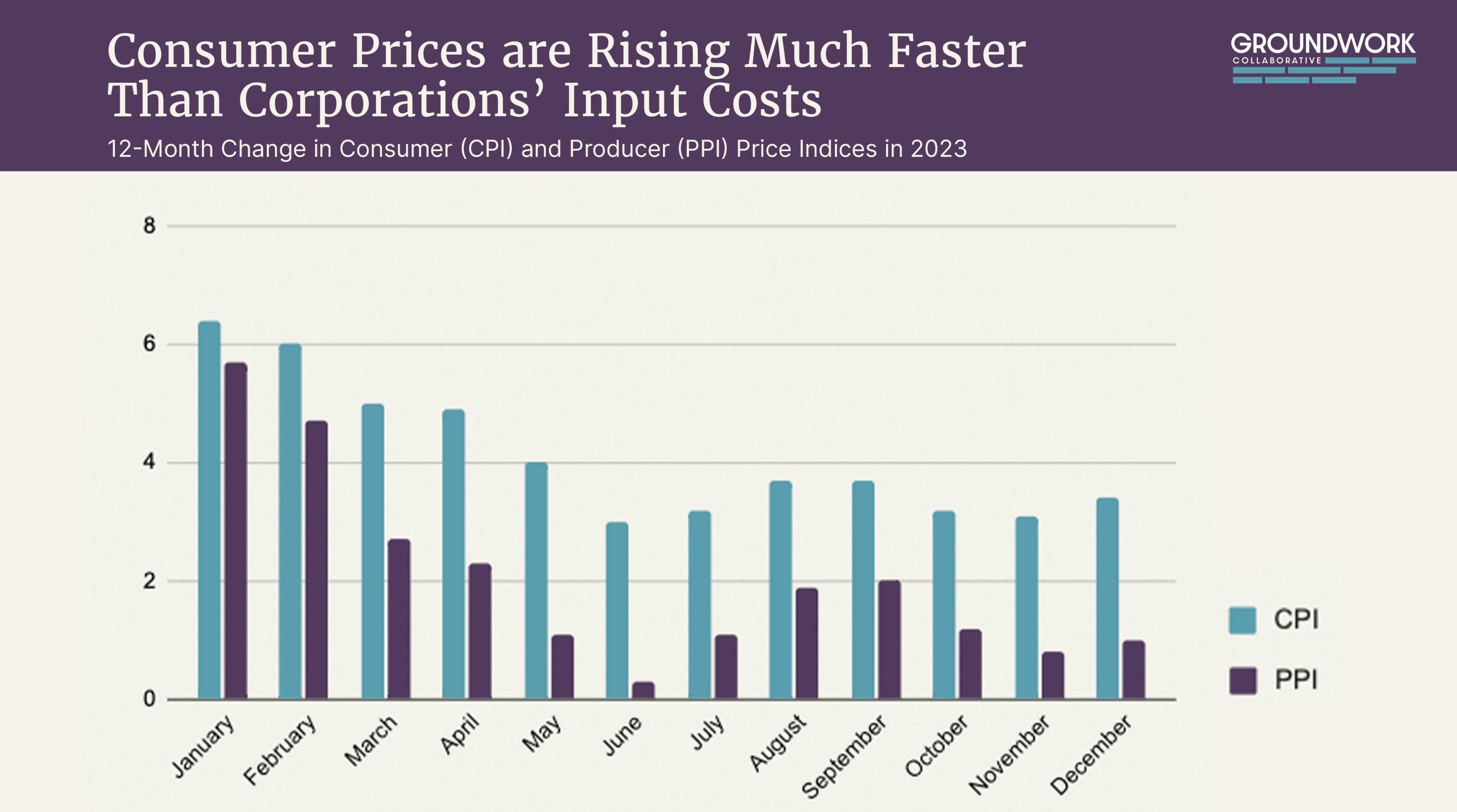

Of course, economic events as complicated as the past four years have reflected a mix of factors. Some of the inflation was demand-driven by massive pandemic relief from the federal government and the pent-up demand due to the shutdown of the economy. Interest rate increases should have an effect. But that effect appears modest, at least so far.

I'm not sure that "effect appears modest" is quite the ringing endorsement for such an enormous intrusion into the economy that you might think. Of course, you will respond that you didn't say it was a ringing endorsement.

Also, I'm still not buying that the prices in sectors like food were demand driven. Did we all of a sudden get hungrier?

I'm not sure that "effect appears modest" is quite the ringing endorsement for such an enormous intrusion into the economy that you might think. Of course, you will respond that you didn't say it was a ringing endorsement.

I'm not sure that "effect appears modest" is quite the ringing endorsement for such an enormous intrusion into the economy that you might think. Of course, you will respond that you didn't say it was a ringing endorsement.

Also, I'm still not buying that the prices in sectors like food were demand driven. Did we all of a sudden get hungrier?

some of the price increases were driven by avian flu, which drove the prices of poultry and eggs sky high. And my understanding was that a shortage of drivers was also responsible for price increases.

and of course, there was increased profits to suppliers.

implied by the Fed's minimal role here is the fact that team transitory was actually right. or at the very least a lot more right than the other team.

I always had problems with the transitory story line because the word transitory is kind of nebulous and people were basically allowed to believe it meant any arbitrary time period that was convenient for their position.

To me, transitory just meant not permanent and not structural and would go away on its own, meaning Fed intervention would not be required.

"Interest rates are heading down. Maybe not today, and maybe not tomorrow, but soon, and for the rest of this year (at least).

"Why? Because there are very good reasons for the Federal Reserve, which controls short-term interest rates — that’s how it makes monetary policy — to start reversing the sharp rate hikes it carried out beginning in March 2022. There’s a vigorous debate about whether those rate hikes were excessive, which I’m not going to litigate here. Whatever you think about past policy, the case for cuts going forward is very strong, and I hope the Fed will act on that case."

"Interest rates are heading down. Maybe not today, and maybe not tomorrow, but soon, and for the rest of this year (at least).

"Why? Because there are very good reasons for the Federal Reserve, which controls short-term interest rates — that’s how it makes monetary policy — to start reversing the sharp rate hikes it carried out beginning in March 2022. There’s a vigorous debate about whether those rate hikes were excessive, which I’m not going to litigate here. Whatever you think about past policy, the case for cuts going forward is very strong, and I hope the Fed will act on that case."

Emphasis added.

Smart. Everyone knows the appropriate place to litigate that sort of thing is here.

Randall Wray: “The conventional wisdom is inflation is mostly a demand-side problem, and low growth is mostly a supply-side problem. The reality is it’s the other way around.” https://t.co/jPqGZOLnLZ

The latest information from Japan suggests that in December 2023, its inflation fell sharply for the second consecutive month and that one might conclude the inflation episode is coming to an end. The Bank of Japan made the assumption that this supply-side inflation was temporary and would subside fairly quickly once those constraints eased. And they were right. All the other central banks somehow convinced themselves that the inflation was demand-driven and have been needlessly pushing up interest rates. The experiment is nearly over and I think it is clear that the Japanese path was the sound one. At that point, the New Keynesian academics and officials should resign. After that, as it is Wednesday, we have some music to soothe our souls.

...

The Bank of Japan has for the last thirty years demonstrated that courses in monetary economics provide no knowledge.

The latest information from Japan suggests that in December 2023, its inflation fell sharply for the second consecutive month and that one might conclude the inflation episode is coming to an end. The Bank of Japan made the assumption that this supply-side inflation was temporary and would subside fairly quickly once those constraints eased. And they were right. All the other central banks somehow convinced themselves that the inflation was demand-driven and have been needlessly pushing up interest rates. The experiment is nearly over and I think it is clear that the Japanese path was the sound one. At that point, the New Keynesian academics and officials should resign. After that, as it is Wednesday, we have some music to soothe our souls.

...

The Bank of Japan has for the last thirty years demonstrated that courses in monetary economics provide no knowledge.

Was Japan in the same economic condition as the U.S, though? For instance, here we also saw wages and consumer demand increasing even as prices went up -- was that also true in Japan?

The latest information from Japan suggests that in December 2023, its inflation fell sharply for the second consecutive month and that one might conclude the inflation episode is coming to an end. The Bank of Japan made the assumption that this supply-side inflation was temporary and would subside fairly quickly once those constraints eased. And they were right. All the other central banks somehow convinced themselves that the inflation was demand-driven and have been needlessly pushing up interest rates. The experiment is nearly over and I think it is clear that the Japanese path was the sound one. At that point, the New Keynesian academics and officials should resign. After that, as it is Wednesday, we have some music to soothe our souls.

...

The Bank of Japan has for the last thirty years demonstrated that courses in monetary economics provide no knowledge.

Was Japan in the same economic condition as the U.S, though? For instance, here we also saw wages and consumer demand increasing even as prices went up -- was that also true in Japan?

Over what period of time?

The reason I ask is that the Japan experience has been running counter to mainstream economics for decades.

The reason I ask is that the Japan experience has been running counter to mainstream economics for decades.

It has, which suggests comparing Japan's actions to those of other countries calls for caution, as it's not a very apple-to-apples comparison. I'm skeptical Japan's experience in the post-pandemic period helps us evaluate that of the U.S.

no. you need to show that they're unlike things. and not merely unlike but unlike enough to make comparisons not helpful.

In the United States, we not only had high price increases, but also strong wage growth and strong demand. Those latter two conditions were not true for Japan. I find that to be a significant difference.

no. you need to show that they're unlike things. and not merely unlike but unlike enough to make comparisons not helpful.

In the United States, we not only had high price increases, but also strong wage growth and strong demand. Those latter two conditions were not true for Japan. I find that to be a significant difference.

it's only significant if US inflation was largely demand driven. it wasn't.

If wage growth and demand in the US had looked as it did in Japan, the Fed would have acted differently than it did. There would have been far more debate over raising rates at all, choosing to do so would have been far more controversial, and if they did raise rates they would have not been raised as high for as long.

Does this prove that, given the actual conditions, the Fed acted correctly? No. But central banks do pay attention to demand and wage growth, and pretending they don't doesn't strengthen your argument.

that's not an unreasonable point, I guess, in terms of describing the possible behavior of the mainstream economists at the the Fed. we'll never know.

I'd say, in counter to that, neither demand or wage growth were rising abnormally during this time so how much did those two factors actually play into the Fed's decisions?

I'd say, in counter to that, neither demand or wage growth were rising abnormally during this time so how much did those two factors actually play into the Fed's decisions?

From the minutes of the March 2022 Fed meeting that started the rate increases:

Many participants indicated that their business contacts continued to report substantial increases in wages and input prices that were being passed through into higher prices to their consumers without any significant decrease in demand. Participants commented on a few factors that might lead the high inflation readings to persist, including strong aggregate demand, significant increases in energy and commodity prices, and supply chain disruptions that were likely to require a lengthy period to resolve.

My spot checks of meeting minutes later in 2022 and in 2023 found consistent references to upward pressures on wages.

I'd say, in counter to that, neither demand or wage growth were rising abnormally during this time so how much did those two factors actually play into the Fed's decisions?

From the minutes of the March 2022 Fed meeting that started the rate increases:

Many participants indicated that their business contacts continued to report substantial increases in wages and input prices that were being passed through into higher prices to their consumers without any significant decrease in demand. Participants commented on a few factors that might lead the high inflation readings to persist, including strong aggregate demand, significant increases in energy and commodity prices, and supply chain disruptions that were likely to require a lengthy period to resolve.

My spot checks of meeting minutes later in 2022 and in 2023 found consistent references to upward pressures on wages.

"participants indicated that their business contacts continued to report"

I'm sure you'd agree this is not an effective way of collecting data.

Anyway, that doesn't say anything about rising demand.

Anyway, that doesn't say anything about rising demand.

If you have any quibbles with my perfunctory look at the easily accessible record regarding a question you asked, you’re welcome to comb through the minutes yourself.

From the first paragraph in the first link I posted in this debate:

"Inflation expectations are simply the rate at which people—consumers, businesses, investors—expect prices to rise in the future. They matter because actual inflation depends, in part, on what we expect it to be. If everyone expects prices to rise, say, 3 percent over the next year, businesses will want to raise prices by (at least) 3 percent, and workers and their unions will want similar-sized raises."

I understand those three sentences. I'm not sure what's preventing you from understanding - I guess you need to do more reading.